|

|

|

|

|

Does

market volatility risk a US hard

landing?

Recent

volatility in global financial markets has

left analysts and investors speculating

whether it is being driven by technical

factors or more fundamental shifts

indicating a looming US recession.

Inflation,

rising US unemployment and heightened

geopolitical tensions are considered major

catalysts for the volatility. The unease in

markets was exacerbated by the unwind of the

yen carry trade and swirling questions about

the Magnificent 7 tech companies’ pace of AI

adoption.

In

this episode of The Flip Side, Global Head of

Research Jeff Meli and Global Chairman of

Research Ajay Rajadhyaksha discuss recent

financial market dynamics and debate the

re-emergence of a hard landing for the US

economy.

|

|

|

| |

|

|

|

|

|

|

The

immigration tailwind

Almost

half a million people immigrated into the US

in December, a record that was just the

latest in a series of elevated inflows

stretching back to spring 2022. While the

surge has caused a public backlash and

prompted political measures to curtail it,

immigration has helped boost economic growth. It has helped relieve

post-pandemic labor shortages and has

been one of the factors behind the

strength of the US economy.

-

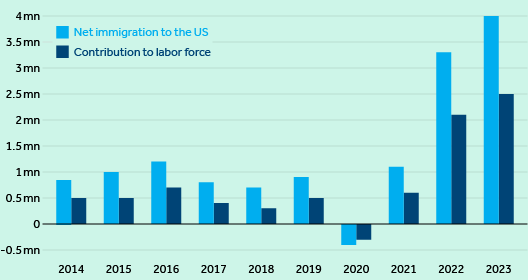

Immigration has

helped ease tight labor

conditions. Net

immigration has increased the US

population by more than 7 million in the

past two years, boosting the labor force

by almost 5 million, according to the

Barclays Immigration Tracker (Figure 1).

That has helped diminish the imbalance

between labor supply and demand that

prevailed following the pandemic. It has

also provided direct reinforcement for

aggregate demand.

-

Immigrants

likely contributed nearly a third of

economic growth. We

estimate that new

immigrants accounted for three quarters

of the increase in private payroll

employment over the past year. Their

contribution of additional hours worked

to output growth more than offset a drag

from US-born workers.

-

Policies

to stem the flow would squeeze the

labor

supply. We estimate that

sustaining the

Biden administration’s recent executive

action that limits inflows of asylum

seekers would trim payroll gains by

almost 1 million in 2025 and lower GDP

growth by half a percentage point, according to our estimates. A

return to former President Trump’s

2017-18 immigration policies could

subtract twice as much from potential

growth in payrolls and economic

output.

Figure

1.

The

recent surge in immigration has boosted the

labor supply

Source:

Department of Homeland Security, Department

of State, US Customs & Border Protection,

Social Security Administration,

Congressional Budget Office, TRAC

Immigration, Barclays Research

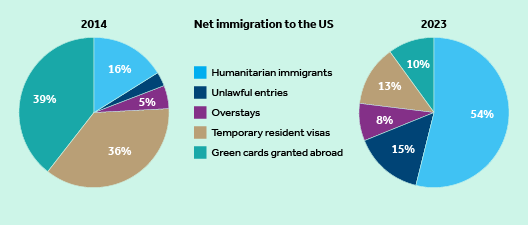

A

surge in asylum seekers

Immigration

to the US takes place in many different

forms. A decade ago, the biggest source of

immigrants was green cards granted abroad.

Today, humanitarian immigrants – asylum

seekers and those invited under various

government programs to escape wars or

natural disasters in their countries – make

up the majority (Figure 2). Asylum seekers typically

qualify for a work permit after a six-month

wait. Unlawful

entries make up only 15% of today’s

inflows, though this share has also grown in

the past decade, according to the Barclays Immigration Tracker. While several million more

enter under temporary work visas every year,

most stay only for the period allowed by

their visas. Thus, their contribution to net

immigration is much smaller.

Computing

net immigration flows is extremely

challenging because there is no centralized

data source. We scoured 14 different sources

to build the Barclays Immigration Tracker,

also adjusting for emigration flows out of

the country. According to our tracker, net

immigration remained relatively stable

between 2014 and 2019, before plunging to

negative territory due to pandemic-era

travel restrictions. Since these were lifted

in 2021, immigration has risen steadily,

reaching an all-time high of 4 million in

2023.

Figure

2.

Humanitarian

immigrants’ share in the total has jumped in

the past decade

Source:

Department of Homeland Security, Department

of State, US Customs & Border Protection,

Social Security Administration,

Congressional Budget Office, TRAC

Immigration, Barclays Research

Immigration’s

boost to the economy

This

recent surge has helped ease the

tight labor market that prevailed following

the pandemic. In its absence, we think that

labor shortages would have been a meaningful

economic headwind, exacerbating wage and

price pressures and requiring a more

restrictive monetary policy stance. Since

2022, when vacancies reached record levels,

jobs have increasingly been filled by

immigrants. By our estimates, such jobs have

accounted for about 75% of the increase in

private payroll employment in the past 12

months.

As

immigrants make up a growing share of

employment gains, they also contribute to a

growing share of output growth. In the first

quarter of 2024, much of the 3.1%

year-on-year growth in output could be

attributed to productivity growth, while 0.9

percentage points was due to hours worked by

immigrants, offsetting the 0.6

percentage-point drag from hours worked by

native born workers.

Policies

to curtail immigration

Both

Democrats and Republicans are campaigning on

policies to slow inflows. We looked at three

scenarios to see the effect of these on

employment and the economy. In the

business-as-usual scenario, where President

Joe Biden’s recent executive order that

attempts to limit substantially the flow of

asylum seekers at the southern border, where

the majority enter, has no meaningful

influence due to judicial intervention or is

circumvented through other means, non-farm

private payroll gains settle at about

208,000 a month in 2025, close to current

levels. In the scenario where the executive

action actually curbs immigration as

intended, we estimate it would subtract

65,000 from the monthly job gains in our

business-as-usual scenario. A return to

2017-18 immigration policies enacted during

the Trump administration would slow monthly

payroll growth by 125,000. That would leave

job growth well below pre-pandemic levels,

as the payroll gains of US-born workers have

fallen sharply in the past decade.

The

US economy’s growth trajectory would differ

under these scenarios as well. The

business-as-usual case points to potential

real GDP growth of 2.6% in 2025. The

intended curbs by the June executive order

and continuation of the same policies in the

next administration could deduct 0.5

percentage points from that potential GDP

growth. The more restrictive immigration

scenario would slow economic growth by

almost one full percentage point.

|

|

|

| |

|

|

|

|

|

|

Water

tech to the rescue

The

world is facing a water crisis. By 2050,

half the urban populations around the world

could face water scarcity. Meanwhile,

efforts to solve the crisis are making

little headway. Technology can provide

solutions, from improving efficiency of use

to harnessing new sources, but investment is

needed to scale the technologies available

or being developed.

The

Eagle Eye talked to Hannah

Greenberg, an

analyst on the Thematic Investing Research

team, about the water crisis and the role of

water tech in helping solve it.

The

Eagle Eye: Why is there a water

crisis?

Hannah

Greenberg:

Water has largely been overlooked compared

with other environmental issues, such as

carbon emissions or climate change; there

have thus been fewer water-specific

policies, and you cannot solve water issues

with those alone. Another challenge is the

low cost of water. We see water as

essentially free. During times of scarcity,

energy prices spike, but water prices have

not despite the crisis. If water prices

spiked like oil prices when supply is tight,

there would be more awareness of its

scarcity and a bigger effort to find

solutions. Even though we derive trillions

of dollars in economic value from water, we

undervalue its contribution to economic

output and have not been doing enough to

address the increasing scarcity and quality

issues around the world. Social and

environmental effects have been better

understood, but the economic side of the

crisis has not been. Companies worldwide

face rising financial risks related to

water.

Eagle

Eye: What kind of risks?

Greenberg:

They face serious operational risks. Many

sectors rely on water for their industrial

processes. If companies do not have water to

run their operations, that will have serious

consequences for their production. For

example, last month during a severe drought

in Mexico, many chemical companies had to

halt production.

Eagle

Eye: How can technology

help?

Greenberg:

There won’t be one silver bullet technology

that solves the water crisis. Instead, we

will need a range of solutions to address

its different elements. Encouragingly, we

are seeing advancements in both mature

technologies and new innovations. We

highlight five key areas: digital water,

precision irrigation, advanced water

treatment & recycling, desalination and

atmospheric water generation (Figure 1). The

scaling of these technologies will be

dependent on location and application, given

cost is a key barrier to adoption. Different

technologies will make the most sense in

different regions. When you are located near

a body of salt water and have cheap energy

sources, desalination makes sense. But if

you are deep inland and energy is expensive,

you have to look at other water tech

solutions.

Figure

1.

Five

major areas where water tech can help

Source:

Barclays Research

Eagle

Eye: What is digital water? It

is not made up of 0s and 1s, is it?

Greenberg:

No, it is not. Digital water is using

technologies such as sensors and artificial

intelligence to make data-driven decisions

about water management. Applications include

smart metering and smart infrastructure,

where digital solutions can catch water

leaks and suggest maintenance in advance so

leaks do not happen in the first place. Many

companies have sustainability targets

including water consumption and discharge

targets. Ecolab is partnering with a lot of

them, providing digital water solutions to

help companies reach their sustainable water

targets.

Eagle

Eye: What is atmospheric water

generation? Can we make water from

air?

Greenberg:

Yes, we can. And the technology is not that

new. Refrigeration-based processes – causing

water vapor to condense and turn to liquid –

has been around for a while. Now, we are

seeing more innovation in novel processes

and sorption, which uses a solid or liquid

dehydrating agent to attract moisture from

the air. Montana Technologies is

commercializing metal-organic framework

technology, using porous polymers to capture

water from the air. Drupps has a system that

traps the water from steam coming out of

factory chimneys while recycling the heat in

the steam into the process. Cost is an issue

in atmospheric water generation; it is more

expensive than other such technologies. But

if you are not in a location where you can

use another technology such as desalination,

atmospheric water generation can be still

cheaper than trucking in water from a

distant source.

Eagle

Eye: Desalination is not new.

It has been used by the Gulf states and

Israel for a long time. Is anything new

there?

Greenberg:

There are new developments on the technology

side driving costs down. There have been

advancements in membranes – what separates

the water from the salt and the minerals –

making them more efficient. It is an

energy-intensive process, so there are

efforts to use renewable energy more. Oneka

Technologies offers wave-powered

desalination: if you are using the ocean as

the source of your water, why not use its

energy to power the process as well?

Eagle

Eye: All this technology will

help us use water more efficiently and

access more clean water. But is it possible

to do some things without water

altogether?

Greenberg:

Yes, indeed. Waterless technologies –

replacing water in industrial processes –

could also help us to reduce our

consumption. Waterless data centers,

waterless cathode manufacturing, waterless

dyeing of textiles: all that is possible and

happening, if slowly. The textile industry

is one of the worst polluters of water and

uses a lot of water to dye fabric, up to 150

liters per kilogram of fabric. DyeCoo has

developed a water-free process, using

pressurized carbon-dioxide instead.

|

|

|

| |

|

|

|

|

|

|

Booking

experiences online

Almost

everyone buys their plane ticket and

reserves their hotel room in advance when

traveling. What they do once at their

destination – the city tour, the museum

visit and the ATV ride in the desert – are

usually done on site and in person. But like

many other things that have shifted more

online since the pandemic, booking

experiences on web sites is now among the

fastest growing segments of the online

travel industry.

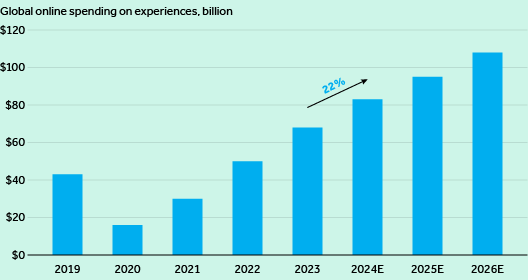

-

Spending on

experiences is likely to

grow. Travelers

already spend quite a lot on tours,

attractions and activities at their

destinations. It was roughly $235

billion last year, making up more than

10% of total travel spending. We expect

experience spending to grow faster than

other segments, reaching $300 billion in

2026.

-

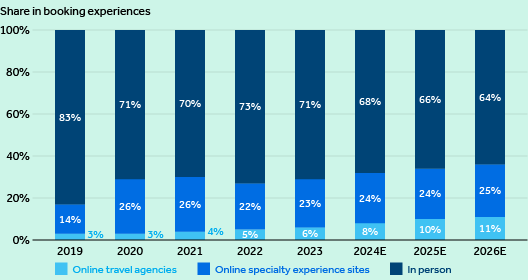

More

people are

booking them online. The

pandemic pushed

people to purchase more goods and

services online, boosting e-commerce.

Travel experience bookings have

benefited from the same trend, helped

by younger generations preferring to do

everything on their smart phones. The

share of experiences booked online has

risen from 17% pre-pandemic to over 30%

this year, a trend that is likely to

rise in the coming years (Figure

1).

-

Online

travel agencies are also in the

game. Specialized platforms

such as

Viator and GetYourGuide make up the bulk

of current bookings. But the leading

online agencies are also offering

experience booking and slowly gaining

market share from the specialized shops.

Airbnb has more than 40,000 local

experiences on offer in over 1,000

cities.

Figure

1.

Booking

experiences online is likely to double this

year from pre-pandemic levels

Source:

Arival, Phocuswright, Barclays

Research

What

to do, what to see

Typically,

many travelers prefer not to have a rigid

schedule while on vacation, opting to book

experiences when they walk up to the

attraction, paying in person. While this has

historically been a hurdle against online

booking adoption, several current trends

make us optimistic about the growth of

online experience bookings. One is the

evolving consumer preference toward more

experience-driven trips and greater

awareness of offerings at a destination. And

even if they do not buy their museum tickets

a month in advance, as they typically would

with their plane ticket, consumers are

booking experiences online at the last

minute to skip the line at the attraction or

a day in advance to make sure they can get

in. This shift is helped by wider smart

phone adoption, and the utilization of

phones as a means to search for what to do

at one’s vacation destination.

Meanwhile,

more operators of tourist experiences are

embracing online booking platforms to help

manage peak/trough demand better. For small

operators, being on the online booking site

adds visibility and provides incremental

business. As more supply comes online,

making it easier to find and book

experiences, it will likely increase

frequency and adoption.

The

experience specialists

The

online experience booking is a highly

fragmented market. The biggest company,

Viator, has about a 5% market share,

followed closely by GetYourGuide. Viator,

which was acquired by Tripadvisor in 2014,

has an inventory of more than 350,000

experiences from 55,000 operators globally,

though it is more focused on North America.

GetYourGuide is stronger in European

experiences, while Hong Kong-based Klook

prioritizes Asia even though it offers experiences

globally.

The

large online travel agencies have also been

involved, although the experience portion

has not yet become a significant contributor

to their bookings or revenues. Booking.com,

Expedia and Airbnb do not disclose how much

the experience business generates for them.

Our estimate is that the share of online

travel agencies in total experience booking spend was about 6% last year, but

we expect it to almost double in the next

three years as they take advantage of

cross-selling experiences to their customers

already booking their flights or stays at

their sites (Figure 2).

Figure

2.

As booking experiences shift online, travel agencies are gaining share

Source: Phocuswire, Skift, Barclays Research

|

|

|

| |

|

|

|

|

|

|

|

|

© 2024 Barclays Bank PLC. All rights reserved. Barclays

is a registered trademark of Barclays PLC, used under

license. Registered office: 1 Churchill Place, London E14

5HP, United Kingdom.

barclays.com/ib

|

Disclosures

|

Privacy

Policy

|

|

|

|

|

|

|

|

|